2 months ago

34

2 months ago

34

Applying First-Order Volatility Trade to MSTR

Navigating Volatility with Precision

MicroStrategy (MSTR) isn’t just another tech stock; it’s a high-volatility beast with a portfolio tethered to Bitcoin. This potent cocktail of stock price swings and crypto-market turbulence makes it the perfect playground for a first-order volatility trade. This strategy isn’t about betting whether MSTR rises or falls; it’s about profiting from the chaos itself—leveraging volatility as your ally.

First-order volatility trading revolves around two key instruments: vanilla options and the principles of delta neutrality. Whether you’re betting on volatility increasing or decreasing, your trade setup determines how you manage risk and reap profits. In this guide, we’ll explore how to deploy these tactics effectively with MSTR as your battlefield.

The Foundation: What is First-Order Volatility Trading?

A first-order volatility trade aligns with these principles:

1. Volatility as the Asset: Betting either for (long) or against (short) volatility, not stock direction.

2. Consistent Vega and Gamma Positioning: Both metrics align on the same side of the market, ensuring the trade behaves predictably under volatility.

3. Delta Neutrality: Neutralize directional bias by rebalancing delta dynamically as stock prices shift.

MSTR’s notorious volatility—driven by its heavy Bitcoin exposure—makes it an ideal candidate for such strategies.

Choosing Your Weapon: Long vs. Short Volatility

Your goal dictates whether you opt to ride the volatility wave or brace for calm waters.

Long Volatility: Profiting from Turbulence

Best for: Expecting large price swings in either direction.

Strategies:

1. Long Straddle: Buy both a call and a put at the same strike price and expiration. Profitable if MSTR moves significantly, up or down.

2. Long Strangle: Buy a call and a put at different strike prices. Less costly than a straddle but requires more substantial price movement.

Short Volatility: Betting on Stability

Best for: Believing MSTR will remain range-bound.

Strategies:

1. Short Straddle: Sell both a call and a put at the same strike price and expiration. Profitable if MSTR doesn’t move much.

2. Short Strangle: Sell a call and a put at different strike prices. Reduces risk compared to a straddle by widening the breakeven points.

Executing the Long Straddle on MSTR

Let’s assume you anticipate a surge in MSTR’s volatility due to an upcoming earnings call or macroeconomic catalyst.

Example Setup

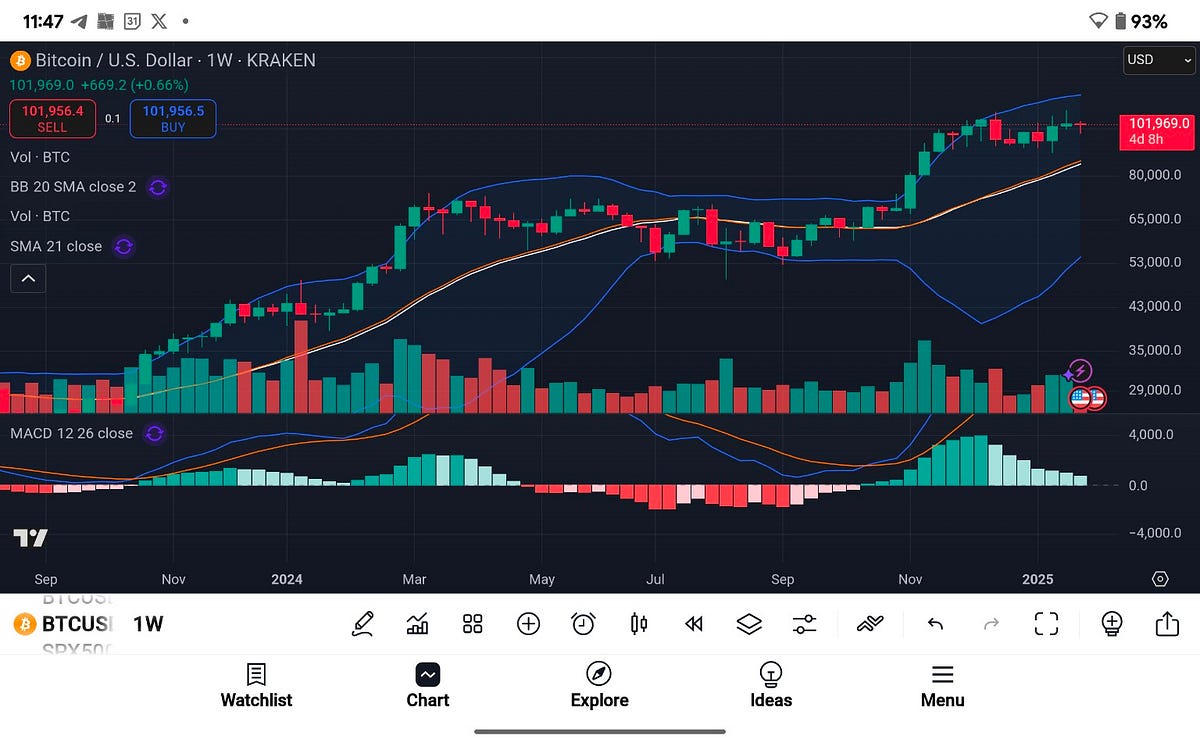

1. MSTR Current Price: $370.

2. Strike Price: At-the-money (ATM), $370.

3. Expiration: 1 month (aligned with expected volatility spike).

4. Volatility Assumption: MSTR’s implied volatility is high, but you expect it to rise further.

Steps to Construct the Trade

1. Buy a Call Option:

- Strike: $370.

- Premium: $30.

2. Buy a Put Option:

- Strike: $370.

- Premium: $25.

3. Total Cost: $55 per contract (100 shares per contract).

Profitability Analysis

Breakeven Points:

- Lower breakeven: $370 - $55 = $315.

- Upper breakeven: $370 + $55 = $425.

Profit Potential:

- If MSTR drops to $300: The put appreciates significantly, covering the premiums and generating profit.

- If MSTR rises to $450: The call appreciates significantly, with similar results.

Dynamic Rebalancing: Delta Neutral Adjustments

Delta neutrality is the linchpin of first-order volatility trading. Here’s how to maintain it:

Delta Explained

Delta measures the sensitivity of your options to stock price changes. For example:

- A call option with a delta of 0.5 means the option’s value increases by $0.50 for every $1 move in the stock price.

- A put option with a delta of -0.5 behaves inversely.

Dynamic Rebalancing

As MSTR Rises:

- The call’s delta increases (more stock-like).

- Adjust by shorting stock to hedge.

As MSTR Falls:

- The put’s delta increases.

- Adjust by buying stock to hedge.

This constant rebalancing ensures the position remains indifferent to directional movements while exploiting volatility.

An Alternative Approach: Short Volatility Trade

If your outlook suggests that MSTR will remain range-bound, consider shorting volatility instead.

Example: Short Strangle

1. Sell an Out-of-the-Money (OTM) Call:

- Strike: $400.

- Premium: $20.

2. Sell an OTM Put:

- Strike: $340.

- Premium: $15.

3. Total Premium Collected: $35 per contract.

Risk and Reward

- Profit Potential: If MSTR stays between $340 and $400, you pocket the premiums.

- Risk: Significant losses if MSTR breaks out of this range, as both options carry unlimited risk beyond the breakeven points.

Key Metrics to Monitor

A successful volatility trade hinges on understanding the following:

Implied Volatility (IV)

- High IV: Favorable for short volatility trades.

- Low IV: Favorable for long volatility trades.

Gamma

- Measures how delta changes with price movements.

- High gamma: Opportunities for frequent adjustments, ideal for long volatility trades.

- Low gamma: Less dynamic hedging, suitable for short volatility trades.

Theta Decay

- Represents the loss of option value over time.

- Works against long volatility positions (you lose premium value daily).

- Works in favor of short volatility positions (you gain as options decay).

Practical Execution Tips

1. Avoid Slippage: Use tight bid-ask spreads to minimize entry/exit costs.

2. Liquidity Considerations: MSTR’s options may have limited liquidity; size your trades accordingly.

3. Timing: Align your trade with known catalysts (e.g., earnings reports) to maximize volatility impact.

Scenario Analysis: Profit from Chaos

If MSTR Drops to $300:

- The put increases in value significantly.

- Adjust the short position to maintain delta neutrality.

- Pocket gains by rebalancing at lower prices.

If MSTR Rises to $450:

- The call surges in value.

- Adjust the short position accordingly.

- Capture profits through dynamic hedging.

If MSTR Stagnates:

- For a long volatility trade, stagnation is detrimental as options lose value (theta decay).

- For a short volatility trade, you profit as the options expire worthless.

The Edge: Why This Works

MSTR’s volatility, driven by its Bitcoin exposure, provides fertile ground for first-order volatility trades. The strategy leverages frequent price swings, capturing value from every move, whether up or down. It’s a methodical, data-driven approach to turning market chaos into consistent profits.

Final Thoughts

Volatility isn’t just noise; it’s an asset class waiting to be harnessed. First-order volatility trades strip away the guesswork of directional bets, replacing them with a strategy rooted in mathematical precision. Whether you’re riding MSTR’s wild swings with a long straddle or banking on calm waters with a short strangle, the key is understanding delta, gamma, and theta dynamics.

Play option with MSTR was originally published in The Capital on Medium, where people are continuing the conversation by highlighting and responding to this story.

English (US) ·

English (US) ·