1 hour ago

15

1 hour ago

15

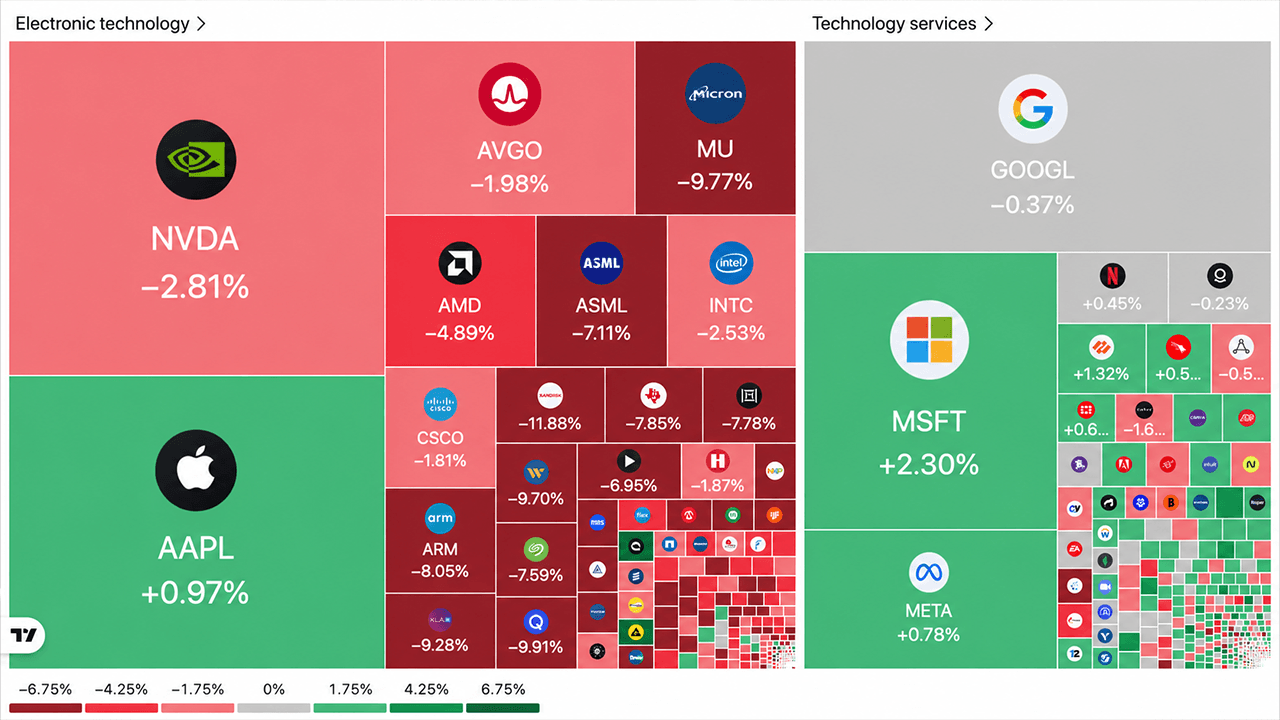

Polymarket bettors are giving Micron Technology a 96% chance of topping Wall Street’s earnings expectations when the chipmaker reports fiscal Q3 2026 results on Wednesday. The prediction market is essentially treating an earnings beat as a foregone conclusion.

The confidence isn’t exactly irrational. Micron has beaten or met EPS estimates in 16 of its last 18 quarters, an 88.89% success rate. But when a market prices something at 96%, the interesting question stops being “will they beat” and starts being “what happens next.”

The numbers Wall Street is watching

Micron’s earnings call is scheduled for after market close on June 24, with a conference call set for 2:30 p.m. MT. Analyst consensus places non-GAAP EPS somewhere between $20.20 and $20.98, with revenue expected to come in above the company’s own guidance of $33.5 billion, give or take $750 million.

To appreciate how wild those numbers are, consider last quarter. Micron posted Q2 2026 revenue of $23.86 billion, which represented 196% year-over-year growth. EPS landed at $12.20.

Micron makes high-bandwidth memory, or HBM, and dynamic random-access memory, known as DRAM. Both are critical components in the AI infrastructure buildout that has consumed the semiconductor industry over the past two years.

Why Polymarket’s odds tell a familiar story

The 96% figure on Polymarket isn’t an outlier. In recent quarters, similar prediction markets for Micron earnings beats have ranged from 95.9% to 97.75%.

Polymarket is a blockchain-based prediction market where users trade on the outcomes of real-world events, which tends to produce more honest probability assessments than opinion polls or analyst sentiment surveys.

What actually matters for investors

Analysts aren’t just watching the EPS print. They’re focused on forward guidance and gross margins, with expectations running near 81% on the margin front. If margins come in below that threshold, even a headline earnings beat could trigger selling pressure.

Analyst upgrades from firms like Needham and Bernstein in recent weeks have added fuel to an already bullish sentiment. The semiconductor supply environment remains tight, and AI infrastructure spending shows no signs of slowing down.

The flip side is worth considering. That remaining 4% probability of a miss might be underpriced. Micron’s last 18 quarters include two misses, which means roughly one in nine reports has disappointed. A 4% miss probability implies something closer to one in 25.

For investors holding Micron shares through the report, the real risk isn’t the headline number. It’s the commentary around HBM supply commitments, pricing trends for the back half of 2026, and whether customers are showing any signs of pulling back on AI infrastructure orders.

Disclosure: This article was edited by Editorial Team. For more information on how we create and review content, see our Editorial Policy.

English (US) ·

English (US) ·