1 hour ago

20

1 hour ago

20

The US leveraged ETF market has ballooned to a record $198 billion in assets under management, a milestone that says as much about investor appetite for risk as it does about the AI-fueled bull run powering it. That figure is up from roughly $170 billion at the end of 2025, a nearly 16% jump in about six months.

Two funds are doing most of the heavy lifting: ProShares UltraPro QQQ (TQQQ) and Direxion Daily Semiconductor Bull 3X Shares (SOXL). Both offer 3x daily leveraged exposure.

The two titans of leveraged trading

TQQQ, which tracks three times the daily return of the Nasdaq-100, sits at the top of the leveraged ETF food chain with assets in the range of $29 billion to $39 billion depending on the reporting date. It remains the single largest leveraged ETF in the US by a comfortable margin.

SOXL isn’t far behind in terms of cultural cachet, even if its asset base is smaller. The semiconductor-focused fund holds between $13 billion and $28 billion, with that wide range itself telling you something about how violently these products can swing. SOXL has posted year-to-date returns exceeding 50% in 2026, riding the wave of insatiable demand for chips tied to AI infrastructure buildouts.

The broader leveraged equities segment accounts for approximately $157 billion of the total, while all leveraged products combined, including those tracking bonds, commodities, and other asset classes, push the total somewhere between $200 billion and $213 billion by some measures.

A long road from $30 billion

To appreciate how far this market has come, rewind to 2009. Total leveraged ETF assets sat at around $30 billion. The sector was a niche playground mostly used by day traders and a handful of hedge funds looking for tactical short-term exposure.

Now it’s a $198 billion industry. That’s roughly a 6.6x increase over 17 years, with much of the acceleration happening in the last few years as retail trading exploded and platforms like Robinhood made access to these products trivially easy.

Leveraged ETFs are designed to reset daily, which means their returns over longer periods can diverge significantly from what you’d expect by simply multiplying the index return by three. In English: if the Nasdaq-100 goes up 10% over a month, TQQQ won’t necessarily go up 30%. Compounding effects, especially in choppy markets, can eat into returns or amplify losses in ways that surprise investors who didn’t read the fine print.

Regulators have repeatedly flagged this distinction. These products are built for short-term trading, not buy-and-hold investing. Yet the record AUM numbers suggest that plenty of investors are treating them as core portfolio positions anyway.

The same reports showing record inflows also note substantial outflows during certain periods, a pattern consistent with traders getting spooked by sudden drawdowns and bailing at the worst possible moment.

What this means for investors

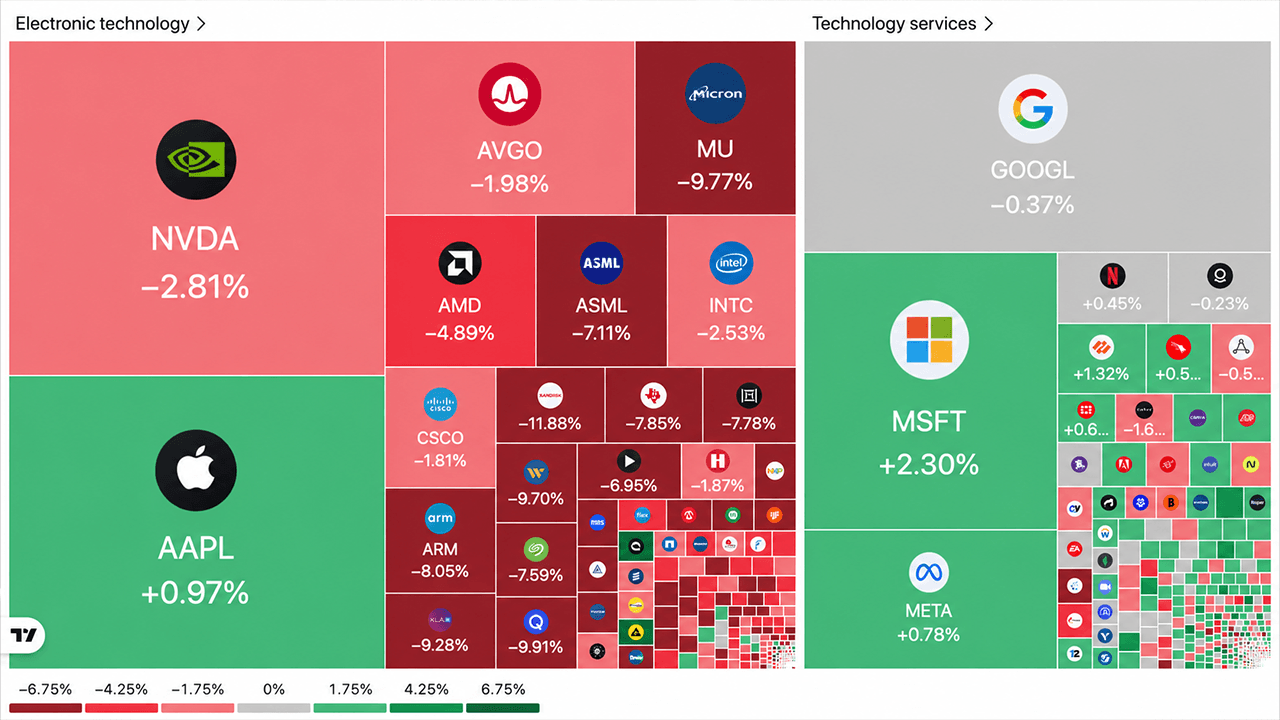

TQQQ and SOXL are both heavily exposed to a relatively narrow set of technology and semiconductor names. If the AI spending cycle hits a speed bump, or if semiconductor inventories start building up faster than expected, these funds won’t just decline. They’ll decline at three times the rate.

When leveraged ETFs grow this large, their daily rebalancing trades can amplify volatility. These funds need to buy more exposure at the end of up days and sell on down days, a mechanical process that can exacerbate moves in both directions. With nearly $200 billion in leveraged AUM, those rebalancing flows are no longer trivial.

Disclosure: This article was edited by Editorial Team. For more information on how we create and review content, see our Editorial Policy.

English (US) ·

English (US) ·