3 months ago

48

3 months ago

48

- XRP carries high volatility, making large allocations risky for retirement

- Small exposure may offer upside without significantly impacting portfolio stability

- Best used as a secondary asset, not a core investment strategy

Retirement portfolios, if we’re being honest, are supposed to be a little boring. That’s kind of the point, steady growth, predictable compounding, something you can actually plan around over decades. But then you throw something like XRP into the mix, and suddenly things get… less predictable. The big question is whether an asset that’s seen massive drawdowns in the past really deserves a place in something meant to be stable long-term.

Volatility Makes XRP a Risky Bet

A big part of XRP’s story ties back to Ripple, the company behind its development and adoption. So, investing in XRP isn’t just about the token itself, it’s also a bet that Ripple will successfully push it into real-world use, especially within financial systems. That’s a long-term narrative, and at times, it’s looked promising, but there have also been long stretches where that confidence just… faded.

Take the 2018 to 2020 period, for example. XRP dropped from around $3.84 to roughly $0.14, which is a massive collapse, close to 96%. For younger investors, that kind of hit might be recoverable with time, assuming the asset rebounds eventually. But for someone nearing retirement, that sort of drawdown could do lasting damage to a portfolio, making large allocations to XRP a pretty risky move.

Small Allocations Could Still Make Sense

That doesn’t mean XRP has no place at all in a retirement strategy, it just means it needs to be handled carefully. For investors with a longer time horizon and a higher tolerance for risk, a small allocation might still be reasonable. The key word there is small, not something that dominates the portfolio, but more of a side position.

In a well-diversified setup, with stocks, bonds, and maybe core crypto assets like Bitcoin already in place, XRP could fit in as a minor addition. Some suggest limiting it to a small portion of the crypto allocation itself, which already makes it a small slice of the overall portfolio. That way, if it performs well, you benefit, but if it doesn’t, it doesn’t derail everything.

Upside Potential Keeps XRP Relevant

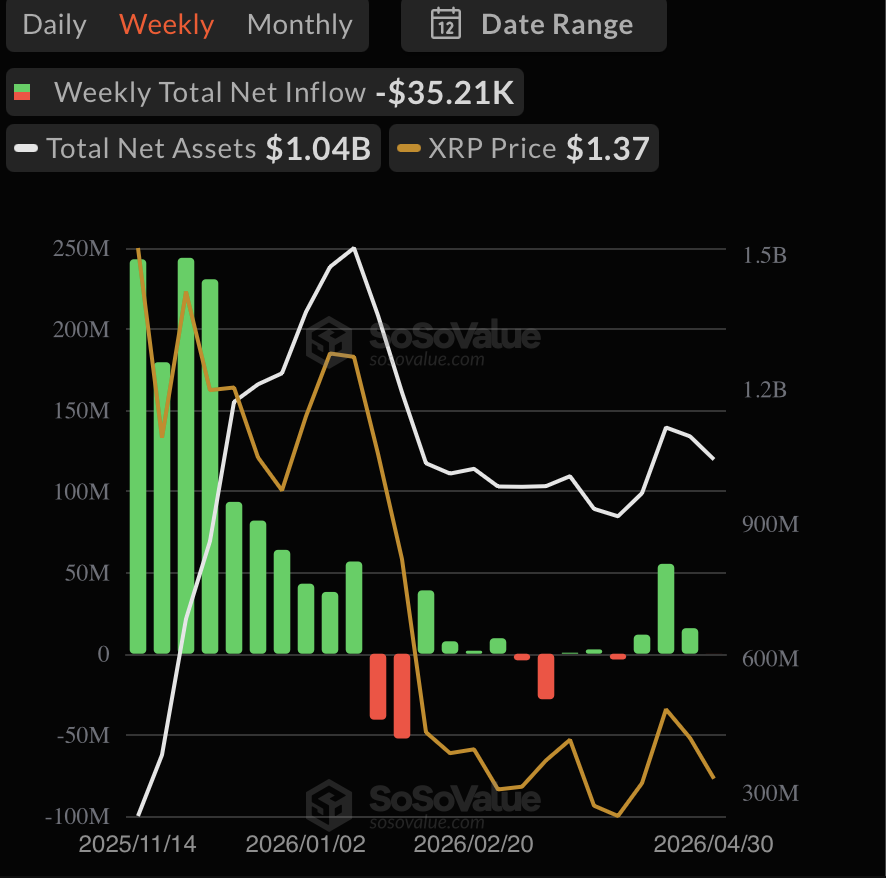

And to be fair, there is upside here. XRP isn’t just a speculative token with no use case, it has ongoing development and growing institutional interest. Spot XRP ETFs have already attracted significant inflows since launching, which signals real demand, not just retail hype. At the same time, the XRP Ledger is being explored for tokenizing real-world assets, which, if it scales, could become a meaningful growth driver.

So there’s a case to be made, just not an all-in case. It’s more of a calculated exposure, something that adds optional upside without carrying too much weight.

A Supporting Role, Not the Foundation

At the end of the day, XRP probably works best as a supporting piece rather than the core of a retirement portfolio. It’s not designed to replace traditional investments like index funds or bonds, which provide the stability most long-term plans rely on. Instead, it sits off to the side, a bit more speculative, a bit more uncertain, but with the potential to contribute if things go right.

And that balance, between risk and restraint, is really what matters here. Too much exposure, and volatility becomes a problem. Too little, and you might miss out, but that’s usually the safer trade-off.

Disclaimer: BlockNews provides independent reporting on crypto, blockchain, and digital finance. All content is for informational purposes only and does not constitute financial advice. Readers should do their own research before making investment decisions. Some articles may use AI tools to assist in drafting, but every piece is reviewed and edited by our editorial team of experienced crypto writers and analysts before publication.

English (US) ·

English (US) ·