4 hours ago

22

4 hours ago

22

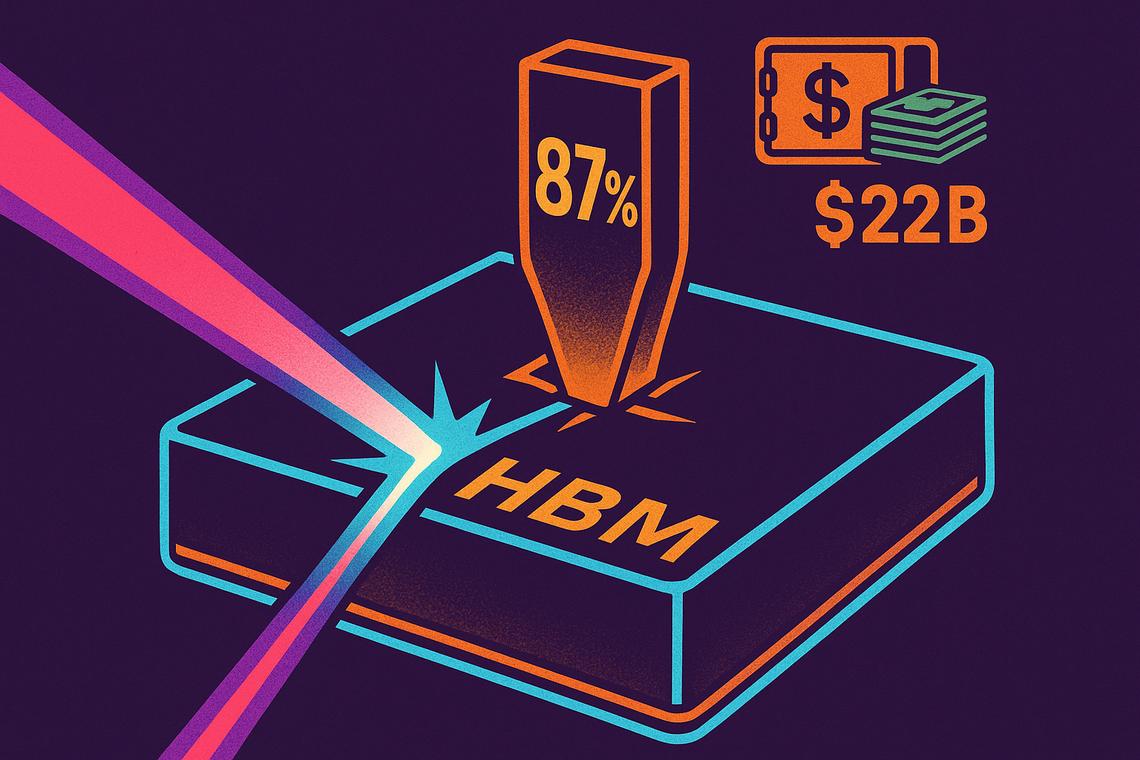

Micron Technology’s data center margins just hit a level that most software companies would envy. The chipmaker posted an 87% gross margin for its data center business in fiscal Q3 2026 — a 12 percentage-point jump from the prior quarter — signaling that the AI memory boom isn’t just a demand story anymore. It’s a pricing power story, and Micron is sitting at the center of it.

Key takeaways

- Micron’s Compute and Data Center Business Unit hit an 87% gross margin in fiscal Q3 2026, up 12 percentage points quarter-over-quarter.

- The unit generated over $25 billion in quarterly revenue, placing it on an annualized run rate north of $100 billion.

- Micron has locked in 16 strategic customer agreements backed by roughly $22 billion in cash deposits, securing future supply commitments.

- Tight HBM supply is rippling into crypto infrastructure costs, particularly for compute-heavy operations like Ethereum scaling solutions.

Micron’s Exceptional Financial Performance in Q3 2026

Numbers like these don’t happen by accident. The 87% data center gross margin Micron reported reflects a market where demand for high-performance memory has structurally outpaced what fabrication lines can deliver — and where Micron has positioned itself directly in the path of that imbalance.

Record Data Center Gross Margins

A 12 percentage-point margin expansion in a single quarter is extraordinary for any hardware business, let alone a semiconductor manufacturer operating at scale. To put it in context: most enterprise software companies consider 80% gross margins aspirational. Micron’s data center unit is now doing better.

The broader business also held up strongly, with GAAP gross margins of 84.6% and non-GAAP margins of 84.9% across all business units — suggesting the data center performance isn’t an outlier pulling up weak results elsewhere, but rather the apex of a company-wide pricing cycle.

Robust Quarterly and Annualized Revenues

Micron’s Compute and Data Center Business Unit generated more than $25 billion in quarterly revenue. Annualized, that puts the unit on a run rate exceeding $100 billion — a threshold that puts it in the same conversation as some of the largest technology businesses in the world.

That’s not just a financial milestone. It’s a statement about how central memory infrastructure has become to the AI buildout reshaping global computing.

Drivers Behind the Margin Boom

The short answer is scarcity. But the mechanics behind it are worth understanding, because they explain why this pricing environment has more staying power than a typical demand spike.

Role of High-Bandwidth Memory and Supply Constraints

Micron’s high-bandwidth memory (HBM), alongside its DRAM and NAND products, sits at the core of every serious AI accelerator and data center server deployment. Every GPU cluster that NVIDIA, AMD, or custom silicon vendors bring online requires massive amounts of high-performance memory — and there simply isn’t enough of it.

The supply gap isn’t easy to close quickly. HBM fabrication involves long lead times and highly specialized production processes. Micron has prioritized HBM output, which tightens supply for other memory segments and lets the company hold pricing across the board. That production prioritization, more than any demand surge on its own, is what’s driving margins toward software-like territory.

Strategic Customer Agreements and Cash Deposits

Perhaps the most telling signal of market dynamics: Micron has signed 16 strategic customer agreements representing roughly $22 billion in cash deposits. Major technology customers aren’t just placing orders — they’re writing billion-dollar checks upfront to secure future supply allocations.

That’s an unusual arrangement in the semiconductor industry, and it speaks to how seriously hyperscalers and AI infrastructure builders are treating memory availability as a strategic constraint. When customers pre-pay at that scale, it effectively validates the pricing environment and de-risks Micron’s forward revenue visibility.

Forward Outlook and Market Implications

Q4 2026 Financial Guidance

Micron’s guidance for Q4 2026 projects approximately 86% gross margins overall. The $22 billion in locked-in customer deposits provides a meaningful floor beneath that forecast.

Implications for AI Infrastructure and Crypto Markets

The Micron data center margin story extends beyond semiconductors and into the broader infrastructure stack — including crypto. High-bandwidth memory has become essential for zero-knowledge proof computation, the cryptographic technique underpinning scaling solutions across Ethereum and other Layer 1 networks. As HBM supply stays constrained and prices remain elevated, the cost structure for running compute-intensive crypto operations stays high too.

This is an underappreciated connection. The same supply squeeze that’s delivering extraordinary margins to Micron is effectively a cost headwind for crypto protocols that depend on ZK-proof computation. Ethereum scaling infrastructure, in particular, becomes more expensive to operate in a world where premium memory commands premium prices.

Customers Gaining Advantage in Supply-Constrained Environment

The competitive implications are stark. Protocols and projects that have already secured hardware partnerships or locked in memory capacity are operating from a position of strength. Those still competing on open markets face higher costs and uncertain availability.

The $22 billion in Micron’s strategic customer deposits isn’t just a financial metric — it’s a map of who anticipated this environment early enough to act. In a supply-constrained AI infrastructure cycle, that kind of foresight translates directly into competitive advantage, whether the operator is a hyperscaler building GPU clusters or a crypto project scaling its ZK-proof infrastructure.

With Q4 guidance holding margins near 86%, the question isn’t whether Micron’s pricing power is real — the numbers confirm it is. The more interesting question is how long the fabrication constraints that created this environment persist, and which players in the AI and crypto ecosystem have already secured their position before the next supply wave arrives.

FAQ

What caused Micron’s data center gross margin to reach 87% in Q3 2026?

Supply constraints driven by long HBM fabrication timelines and Micron’s deliberate prioritization of high-bandwidth memory production created a highly favorable pricing environment, pushing data center gross margins to 87% — a 12 percentage-point increase from the previous quarter.

How significant is Micron’s data center revenue performance?

Micron’s Compute and Data Center Business Unit generated over $25 billion in quarterly revenue in fiscal Q3 2026, placing the unit on an annualized revenue run rate exceeding $100 billion — a scale that ranks it among the largest technology businesses globally.

What role does high-bandwidth memory (HBM) play in crypto infrastructure costs?

HBM is increasingly critical for zero-knowledge proof computation, which underpins scaling solutions for Ethereum and other Layer 1 networks. With HBM supply tight and prices elevated, the cost of running compute-heavy crypto infrastructure rises in parallel with Micron’s margins.

How does the supply environment affect Micron’s customers?

Customers who secured supply early through strategic agreements — including the 16 deals backed by roughly $22 billion in cash deposits — are better positioned than those competing on open markets, where limited availability and high prices reduce flexibility and increase operational costs.

Article produced with the assistance of artificial intelligence and reviewed by the editorial team.

English (US) ·

English (US) ·